Say, Dwello to smarter home loans.

We're a small, family-run mortgage brokerage making finance simple, strategic and hassle-free

What Sets Us Apart

We Think Beyond the Approval

We don't just help you get a loan, we help you build a smarter future.

Most brokers focus on getting a deal done. We focus on what happens next. Whether you're buying your first home, upgrading later or planning to invest - we structure your loan to support your long-term goals.

Because a smart loan today, creates better opportunities tomorrow.

We're Available When It Matters Most

Because real estate doesn't stop at 5pm.

Spotted your dream home at a Saturday open house? Need answers late in the evening? We’re here for it. That’s the beauty of working with a small, family-owned and run mortgage brokerage - we work for ourselves, not someone else.

We don’t clock off at 5pm like the big brokerages do. When you reach out, you’re speaking directly to the owners and we're here to help you move fast, with clear answers and real support, whenever you need it.

We're Personal

Real people. Real support. Family-owned, no call centres.

We're Strategic

We structure loans for long term growth.

We're Available

Weeknights, weekends - we're here when others aren't.

We've Been There

We know the stress of buying - so we've made it easier.

What We Help With

First home loans

Upgrading or upsizing

Investment lending

Strategic refinancing

Complex lending structures

Ongoing lending support

Meet Hannes

Your Broker & Strategic Guide

Originally from Germany, Hannes moved to Australia over a decade ago and has built a career helping people make smarter financial moves. With over 8 years in the finance industry, Hannes brings deep knowledge, real-world experience and a genuine passion for helping people succeed.

He started out in the asset finance space but quickly realised he wanted to offer more (not just loans for depreciating assets), but real value through long-term financial strategy. With his industry expertise and problem-solving mindset, Hannes made the shift to mortgage broking to help clients build wealth and move toward their bigger goals.

Hannes believes the Australian dream isn’t out of reach - even in tough times. It just takes the right steps, the right structure and someone who genuinely cares about your outcome.

You might not start exactly where you want to be, but with the right plan, you can absolutely get there.

As a passionate, dedicated and approachable small business owner, Hannes is here to guide you with honest advice, clear communication and a strategy that works for your future.

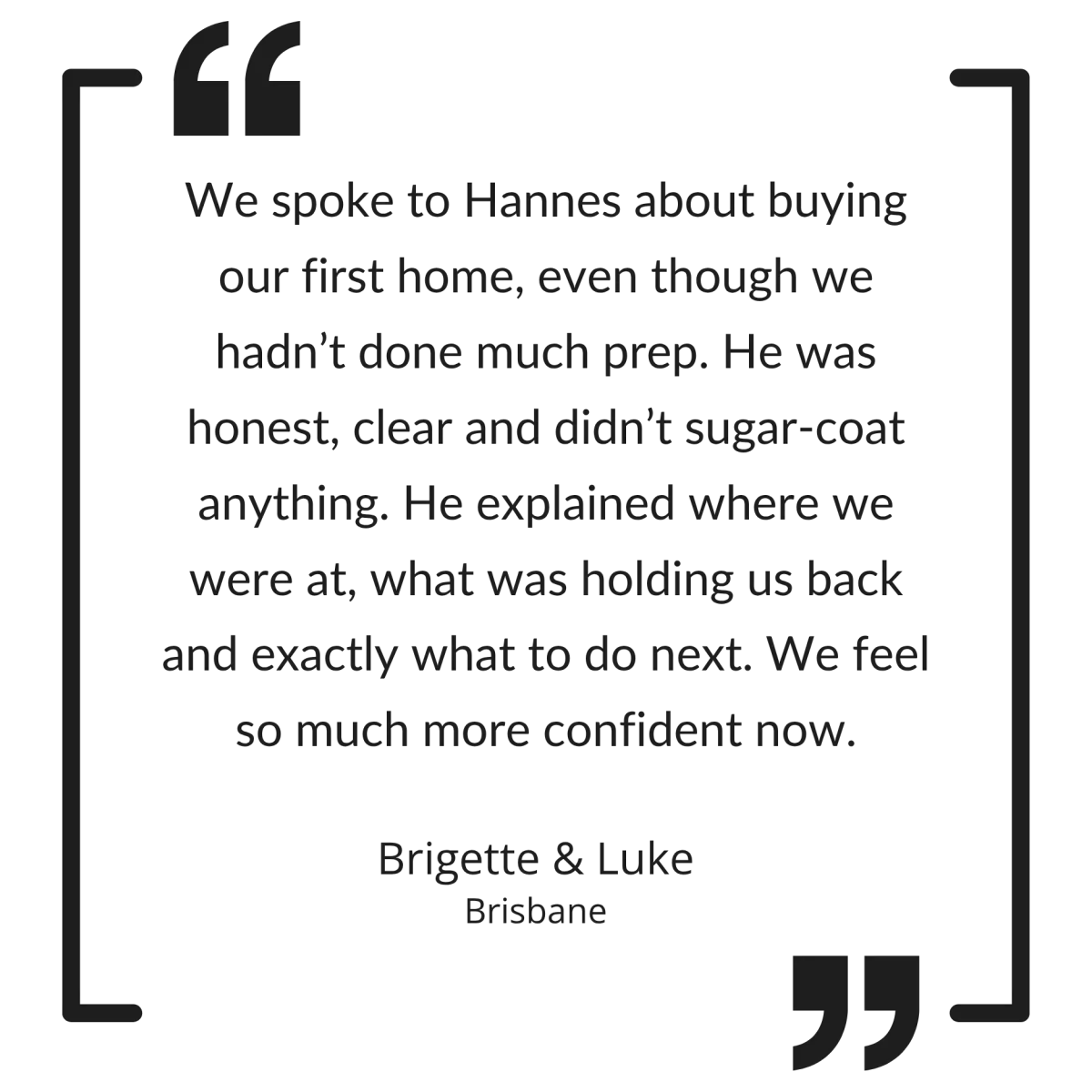

Real Client Testimonial

Our Most Frequently Asked Questions

How much deposit do I need for a home loan?

Most lenders typically require about a 20% deposit of the property’s price for a home loan. If you have less than a 20% deposit, you will generally need to pay for Lender’s Mortgage Insurance (LMI), which protects the lender if you default on the loan. Some first-home buyer programs and lenders allow smaller deposits (sometimes 5–10%), but these often come with extra costs or conditions (for example, paying LMI, using a family guarantor or qualifying for a government scheme).

Do I need pre-approval before house hunting?

While it’s not legally required, we strongly recommend getting pre-approval before you start looking. It gives you a clear idea of your borrowing capacity, helps you make stronger offers, speeds up the finance process and uncovers any potential issues early - like credit or policy mismatches. Without it, you risk delays or disappointment if your loan can’t be approved in time. Pre-approval isn’t a guarantee, but it’s one of the smartest first steps you can take to house hunt with confidence.

How much can I borrow (what is my borrowing capacity)?

Your borrowing power depends on your financial situation and each lender’s criteria. Lenders will assess factors such as your income, your regular living expenses and any existing debts or financial commitments, as well as your credit history and credit score. In general, the more income you earn (and the fewer expenses and debts you have), the more you can borrow. Keep in mind lenders also apply a “serviceability buffer” – they test your ability to make repayments at an interest rate a few percentage points higher than the current rate, to ensure you could still afford the loan if rates rise.

Should I choose a fixed or variable interest rate loan?

This is a very common question. With a fixed interest rate, your rate is locked in for a set period (e.g. 1–5 years), so your monthly repayments stay the same during that time. This stability makes budgeting easier. With a variable interest rate, the rate (and your repayments) can move up or down over time as market interest rates change. Variable loans often offer more flexibility, for example, many allow extra repayments or have an offset account to help reduce interest. Some borrowers also choose to split their loan (part fixed, part variable) to get the security of a fixed rate on a portion and the flexibility of a variable rate on the rest.

How does refinancing my home loan work and when should I consider it?

Refinancing means switching your current home loan to a new loan, either with your existing lender or a different lender - usually to get a better deal. Many borrowers refinance to secure a lower interest rate, reduce their monthly repayments or to access equity (cash out some of the home’s value for renovations, investments, etc.). Refinancing can save you money over time if you find a cheaper rate or more suitable loan features. However, it’s important to consider the costs of refinancing, for example, you might face exit fees or break costs on your current loan and upfront application or settlement fees on the new loan. You should only proceed with refinancing if the overall benefit (e.g. interest savings) outweighs these costs.

Should I get an interest-only loan or principal and interest loan?

With a principal-and-interest (P&I) loan, each repayment covers the interest due and pays down part of the loan principal, so you are gradually reducing your debt over time. In contrast, an interest-only loan (for an initial period, say 5 years) means your payments cover only the interest charges and do not reduce the principal - your outstanding loan amount stays the same during that interest-only period. An interest-only loan gives you lower monthly repayments at first (since you’re not paying off the principal), which can help with cash flow. This is why property investors often use interest-only loans. However, there are trade-offs: because you’re not reducing the balance, you’ll end up paying more interest overall in the long run and after the interest-only period ends, your repayments will jump up (since you then have to start paying off the principal, usually over a shorter remaining term).

Brisbane based

But we service Australia wide

Available 7 days a week

Yes, even on weekends and after hours